We use some essential cookies to make our website work properly.

We’d also like to set additional cookies to help us improve our website, tailor marketing and provide a more personal experience.

Most people spend their working lives looking forward to retirement. But for a growing number of people across the UK, a comfortable retirement is becoming harder to achieve.

The Pensions and Lifetime Savings Association (PLSA) sets a national benchmark for what a comfortable retirement looks like. While this is a useful starting point for saving, national averages don’t account for where you live. This is a factor that can dramatically change what retirement actually costs.

In some UK cities, the annual spend required for a comfortable retirement now exceeds the median full-time local salary. Even the full State Pension covers less than a third of what most people need. For some individual retirees, that might mean searching for work long after they expected to have stopped.

The team at Key Group analysed retirement costs across 10 major UK cities to understand the scale of the regional retirement divide. What it reveals is that the range of options people may need to consider is broader than many expect, from pension savings to property-based options like equity release.

The PLSA has developed a framework called the Retirement Living Standards. It sets out three tiers of retirement lifestyle - minimum, moderate and comfortable - based on real spending data.

According to the PLSA's 2025 update, a comfortable retirement costs £43,900 per year for a single person. That includes regular meals out, an active social life, UK and European holidays, and the ability to replace household goods when needed.

The Standards draw from national averages to help people understand what retirement income they might need. What it doesn’t account for is that where you live has a notable effect on what retirement actually costs.

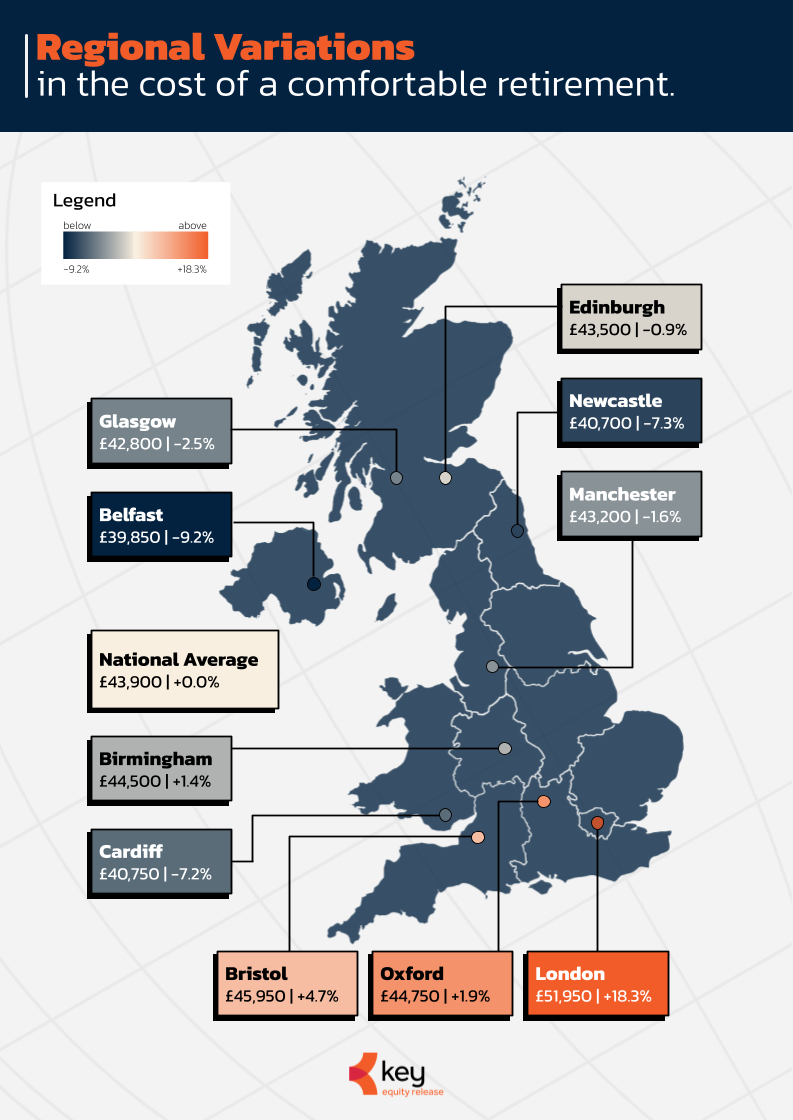

For example, a single retiree in London may need more than £51,950 a year to maintain a comfortable lifestyle. In Belfast, that figure is closer to £39,850.

This is what’s known as the regional retirement divide. It's a gap that has real consequences for how much people need to save, and it varies considerably depending on where you live.

Key analysed retirement costs in 10 major UK cities, using the core spending categories defined by the PLSA framework. These include household bills, food and dining, transport and leisure. Our research identifies where and by how much local costs differ from the national baseline.

What we found is that the differences are considerable. A single retiree in London may need £51,950 per year to maintain a comfortable lifestyle. In Belfast, the same lifestyle costs around £39,850. That's a gap of £12,100 a year, simply based on location. Over a typical 20-year retirement, that location premium could amount to more than £242,000 in total spending.

Retirement costs by city (2025/2026):

| City | Single Total | Difference from Average |

|---|---|---|

| London | £51,950 | 18.3% |

| Bristol | £45,950 | 4.7% |

| Oxford | £44,750 | 1.9% |

| Birmingham | £44,500 | 1.4% |

| National Average | £43,900 | 0.0% |

| Edinburgh | £43,500 | -0.9% |

| Manchester | £43,200 | -1.6% |

| Glasgow | £42,800 | -2.5% |

| Cardiff | £40,750 | -7.2% |

| Newcastle | £40,700 | -7.3% |

| Belfast | £39,850 | -9.2% |

Not all costs vary equally across the UK. Our research points to two categories that create the largest differences between cities.

Leisure spending - on holidays, entertainment and socialising - shows the widest range of any category. A retiree in London may spend over £21,850 a year on leisure alone. In Cardiff, that figure is closer to £15,050.

Food and dining costs also vary considerably. London's higher restaurant and grocery prices push that category to £14,200 per year, compared to £11,900 in Newcastle.

The table below breaks this down further across the four main spending categories.

| City | Housing & Tax | Food & Dining | Transport | Leisure |

|---|---|---|---|---|

| London | £12,995 | £14,222 | £2,890 | £21,857 |

| Bristol | £13,538 | £13,563 | £1,582 | £17,279 |

| Oxford | £13,408 | £12,438 | £1,474 | £17,407 |

| Birmingham | £12,713 | £12,162 | £1,318 | £18,319 |

| Edinburgh | £12,078 | £12,596 | £1,366 | £17,466 |

| Manchester | £12,064 | £12,619 | £1,450 | £17,067 |

| Glasgow | £12,087 | £12,399 | £1,330 | £17,008 |

| Newcastle | £12,271 | £11,880 | £1,210 | £15,407 |

| Cardiff | £12,136 | £12,214 | £1,270 | £15,059 |

| Belfast | £10,752 | £12,534 | £1,258 | £15,319 |

Many people expect their State Pension to be the backbone of their retirement income. In reality, it covers far less of the cost of a comfortable retirement than you’d think.

The full new State Pension is £11,973 per year (2025/26) for a single person. That means the State Pension covers less than 28% of the income most single people would need for a ‘comfortable’ retirement. And that’s before location is even factored in. In major cities, the gap is wider still. In London, where a comfortable retirement may cost £51,950 a year, the State Pension covers just 23.04% of required income. In every city we analysed, the State Pension covers less than 30% of what's needed.

That means more than three-quarters of retirement spending must come from other sources. That 'somewhere else' is often a combination of private pension savings, investments or property wealth. For some homeowners, this may include releasing funds tied up in their home through equity release, which may include a lifetime mortgage; a loan secured against your home.

Where you retire affects how large your overall retirement pot needs to be. Understanding your position based on where you retire is a crucial part of planning ahead.

Retirement is often associated with spending less. But in some parts of the UK, the opposite may be true.

In many UK cities, the annual cost of a comfortable retirement now exceeds what the average full-time worker earns. In other words, stopping work may actually require more income than working did.

Data from the Office of National Statistics backs this up. In Cardiff, the median annual pay for all workers is £33,300. Yet a comfortable retirement in the same city is estimated to be £40,750 - around 22% more than the median local worker earns. Similarly in Newcastle, comfortable retirement spending of £40,700 similarly exceeds the regional median salary of £31,900.

Crucially, these are among the more affordable cities in our analysis. That the gap exists here underlines how widespread the challenge is across the UK.

For many people, this means rethinking what 'enough' looks like. A comfortable retirement may cost more than a working salary, so saving plans may need to reflect that.

Moving to a less expensive part of the UK is one way some retirees look to make their savings stretch further. And on the whole, northern cities do tend to have lower overall retirement costs. But the picture is more nuanced than it might appear.

Council tax can catch people out. A Band D property in Wandsworth costs around £1020 a year. In Newcastle, the equivalent is roughly £2,540 - a difference of £1,520.

So, it’s true that a move north may help you save in some areas. But you could end up spending more in others, which may affect how much better off you actually feel.

The rising cost of retirement is having a visible effect on when people choose to retire.

To explore this trend further, Key analysed Google Keyword Planner data covering over 370 work-related search terms from the Oxford region. The results showed that in Oxford, one of the more expensive cities in our analysis, searches for jobs among retirees and pensioners increased by 31% between 2024 and 2025.

This suggests that for some people in high-cost cities, retirement is no longer a clean break from work. Rising costs may be prompting retirees to return to employment, take on part-time work or delay retirement altogether.

Living somewhere with a higher property value doesn't automatically make retirement more secure. In fact, higher living costs can work against you. Some retirees in expensive areas end up under more financial pressure than those in cheaper parts of the UK.

Search data reflects intent, not outcome. But the trend points to a broader truth: the cost of retiring comfortably is catching up with - and in many cases exceeding - what people had planned for.

FCA data shows that pension withdrawal rates have increased by 35.9% when comparing the 2024/2025 to 2023/2024 tax years. This suggests that more people are drawing on their savings more heavily than anticipated.

Regional spending differences and life expectancy can affect how long savings last. Higher local costs mean savings are drawn on more quickly. And with many people retiring today expected to live well into their 80s or beyond based on the ONS life expectancy calculator, a retirement pot that looks enough at 65 may need to last 25 to 30 years.

Understanding your own position clearly is an important first step. A qualified financial advisor can help you in addressing your specific circumstances and planning for the retirement you desire.

Downsizing to a smaller home or relocating to a lower-cost area can be a practical way to strengthen a financial position.

It is worth approaching this as a way to protect yourself financially rather than a last resort. For some people, a carefully considered move can free up capital, reduce ongoing costs and help savings last longer.

That said, moving home is a major life decision. The financial case needs to be weighed against personal priorities like proximity to family, community ties and access to healthcare. What works well for one person may not be the right choice for another. A qualified financial adviser can help determine whether it's the right approach.

For many older homeowners, a significant portion of their wealth is tied up in their home.

According to ONS wealth statistics, property wealth accounts for around 40% of total household wealth in Great Britain. For some people, that makes their home their largest single asset. One that’s easy to overlook when thinking about retirement finances.

One option worth understanding is equity release. This is a way of accessing some of the value tied up in your home without having to sell it or move out. Used carefully, it may help bridge the gap between pension income and the retirement lifestyle you had planned for.

Equity release is not suitable for everyone. It is a long-term commitment that will reduce the value of your estate. It may also impact entitlement to means-tested benefits. Compound interest rolls up over time, which means the amount owed can grow considerably. Always consider the implications and take financial advice before making any decisions.

You can calculate how much you could release to get a clearer sense of what might be possible.

A comfortable retirement costs more than people might expect. And for a growing number of people, the gap between what they have saved and what they may need is wider than they realise.

The State Pension alone is unlikely to support a comfortable lifestyle. Private savings, investments and property wealth will increasingly need to fill the gap. How large that gap is will depend on where you live, how much you have saved in your pension, how long you need your money to last and how costs change over time.

Careful, informed planning means:

There is no single solution that works for everyone. But the earlier and more clearly you understand your own position, the better placed you will be to make decisions that are right for you.

Thinking about your pension and whether you are financially ready to retire? Speaking to a qualified financial adviser can help you understand your options clearly and at your own pace.

This report sets out to answer a simple question: what does a comfortable retirement actually cost in the UK, and does that change depending on where you live?

To find out, we took the PLSA's 2024 research report to define a national ‘comfortable’ retirement budget and adjusted it across four spending categories that typically vary by location. We then applied those adjustments to 10 major UK cities to arrive at a localised estimate for each.

The four variable categories were:

Housing and council tax - using 2025/26 Band D council tax rates for England and Scotland, average domestic rates for Belfast, £245 annual allowance for household insurances, £3,638 for household goods, £2,272 for household services, alongside varying regional utilities costs.

Food and dining out - adjusted from the PLSA food basket of approximately £8762 per year using regional restaurant and grocery price indexes.

Transport - based on PLSA uniform travel costs of £490 with city-specific adjustments for travel card costs.

Leisure activities - covering holidays, entertainment and socialising, adjusted for local prices and ticket costs. All figures are rounded to the nearest £100. The estimates in this report are intended as a guide. Individual circumstances will vary.