We use some essential cookies to make our website work properly.

We’d also like to set additional cookies to help us improve our website, tailor marketing and provide a more personal experience.

Unless you choose to do so, there are no repayments to make on a lifetime mortgage until the plan comes to an end. As a result, you pay interest not only on the loan itself, but also on the interest that’s already been added to the loan. But there are ways you could reduce the total cost of borrowing of your lifetime mortgage which we outline in this guide.

Whether interest is added to your lifetime mortgage on a monthly or annual basis is dependent on your plan. But during that first period, the interest is charged and added to the original loan amount - the sum of tax-free cash you unlock from your home’s value.

Compound interest is calculated by adding interest to the original loan amount and then charging interest on the new total over time. This means interest is calculated on both the initial amount and any previously added interest. With a lifetime mortgage, the rate, loan term, and frequency of compounding can all affect how much is owed. To understand how this might impact your future balance, try our free equity release calculator to see personalised results based on your circumstances.

ⓘ Compound interest example

Illustrative purposes only. It uses the average release amount of £82,475 and monthly equivalent rate (MER) of 6.3% – Key Market Monitor H1, 2023. Average UK house price of £288,000 – ONS, August 2023.

| Year | Balance at start of year | Interest (6.3% MER)¹ | Balance at end of year² | Remaining property equity³ |

|---|---|---|---|---|

| 1 | £82,475 | £5,349 | £87,824 | £200,176 |

| 2 | £87,824 | £5,695 | £93,519 | £194,481 |

| 3 | £93,519 | £6,065 | £99,584 | £188,416 |

| 15 | £198,778 | £12,891 | £211,669 | £76,331 |

| 20 | £272,153 | £17,649 | £289,802* | £0 |

* The end of year balance is higher than the property's value. You'll never owe more than your home's worth, though, with a lifetime mortgage we recommend. This is the no negative equity guarantee.

¹ The rate at which interest adds to the loan – in this case, monthly (MER). All lifetime mortgages we recommend have a fixed interest rate for life. This column shows how much interest has added to the loan that year.

² How much is owed at the end of the year, including compound interest.

³ The difference between your property value and your outstanding lifetime mortgage balance.

All lifetime mortgages we recommend come with features which could help to reduce the total cost of the borrowing if that’s important to you; for instance, if you wish to leave a larger inheritance to your loved ones.

Even though there are typically no monthly repayments to make with a lifetime mortgage, all plans we recommend come with the option to make ad-hoc or regular repayments to help reduce your total cost of borrowing. Even if you’re only able to make small repayments, it will help reduce the amount of interest you pay over the lifetime of your loan.

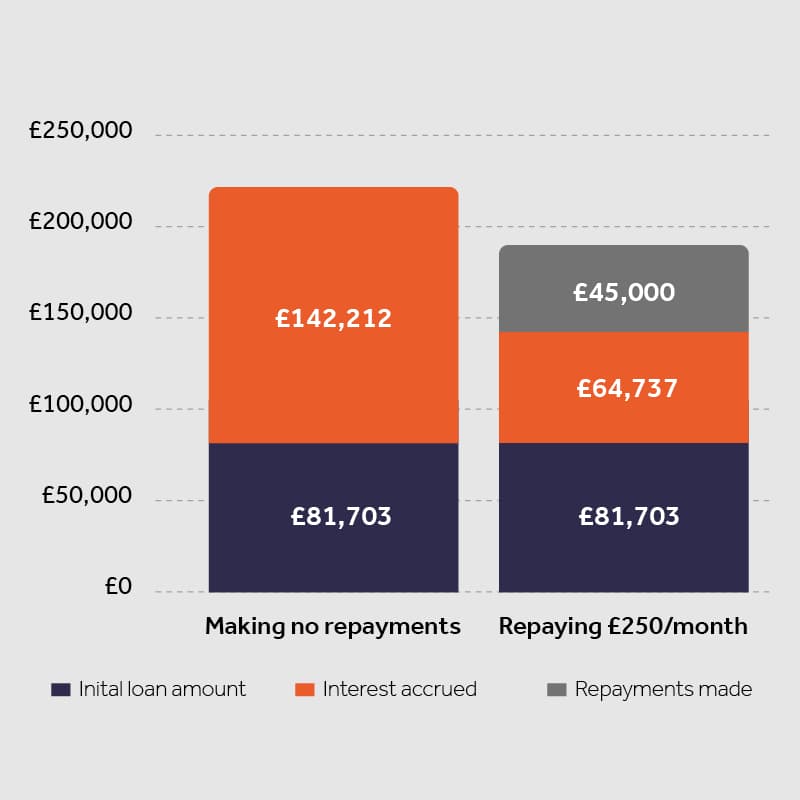

ⓘ Illustrative example

In this example, if you were to borrow £81,703, with a fixed 6.74% MER interest rate, and make no repayments at all, after 15 years, your total cost of borrowing would be £223,915. However, by making a monthly £250 repayment, after 15 years, you’d owe £146,440 - with a total cost of borrowing, including repayments, of £191,440. This means, by repaying £250 a month, you, and your beneficiaries, could benefit from a £32,475 net interest saving.

If interest rates reduce in the future, you may have the option to remortgage your current plan to secure a lower rate.

With a drawdown lifetime mortgage, you only take out the money you need when you need it. This can help reduce your total cost of borrowing, as interest is only charged on the money you release, rather than the full amount available. It's worth noting that a drawdown facility is not guaranteed as the lender has the right to withdraw it. More on lump sum vs drawdown lifetime mortgage

Watch our video to learn more about the benefits and drawbacks of equity release and see if it could be right for you.

All our equity release advice relates to lifetime mortgages - a loan secured against your home.

Video transcript (pdf)

It's a regulatory requirement for anyone considering equity release to get specialist advice before taking out a lifetime mortgage. So why should you choose Key as your equity release company?

ⓘ Did you know...

Over the years, more than a million customers have benefitted from our expert advice, experience and professionalism from Key. We've been rated 'Excellent' on Trustpilot and you can check out the great things our customers have to say about the equity release plans we recommend.

69, Retired

“I sat down with the adviser and he went through every single detail and concerns, plus a lot more which I didn’t know about. They took care of everything… it’s so uncomplicated… the process is so easy.”

Read more on John's experienceYour other options with Key

If another product is more suitable, we'll refer you to a different specialist adviser within Key Group who can help. If you go ahead, you'll never be charged more than our standard fixed advice fee of £1,699, even if their fee is higher. Key offers alternatives to equity release such as a retirement interest-only mortgage or retirement repayment mortgage.

Other options to think about

It's important to know your other options before going ahead with equity release. These include: downsizing, unsecured lending, using existing assets, or support from friends or family.

When it comes to releasing equity from your home, we understand that you may have questions too. To help, we have compiled the answers to the questions we get asked the most. If you are still unable to find the information you're after, we are just a phone call away - and we will have compound interest explained to you in full.

All lifetime mortgages we recommend come with features which could help to reduce the total cost of the borrowing if that’s important to you; for instance, if you wish to leave a larger inheritance to your loved ones.

You can work out compound interest by looking at:

Your starting amount (the loan or savings)

The interest rate

How often the interest is added (monthly, yearly, etc.)

How long the interest is applied for

Compound interest means interest builds on both the original amount and any interest that's already been added. So over time, the amount grows faster than with simple interest.

The easiest way to calculate it is by using a compound interest calculator online — just enter your details and it will do the maths for you.

You may wish to repay some of your lifetime mortgage early and reduce the size of the loan you accrue interest on. Subject to criteria, we may be able to help you personalise your plan with the option of making ad-hoc repayments of up to 10%-12% of the initial amount you've borrowed each year.

Additional repayments, including repaying in full, may incur early repayment charges. Your adviser will explain these terms clearly so you know what your options are.